I often earn from qualifying purchases. This includes Amazon Associates.

How do bankers make money? This is something we ponder yet seldom gain a complete comprehension of.

This complex process is actually quite fascinating and involves more than just holding onto your deposits.

The banking industry, with its intricate web of financial services from commercial to investment banking, operates on multiple revenue-generating strategies.

Digging deeper into how bankers make money, we find layers of interest income, fee-based earnings, and capital market activities contributing to their profits.

The Basics of How Banks Make Money

The secret lies in their ability to offer a myriad of financial services. They are not just safe havens for your cash; they also play significant roles in the economy.

Banks primarily generate revenue through two avenues: commercial banking and investment banking, each having its unique strategies for making money.

Commercial Banking

Commercial banking offers a variety of services, such as checking accounts, savings accounts, credit cards and loans. These offerings form the bedrock upon which most bank operations rest.

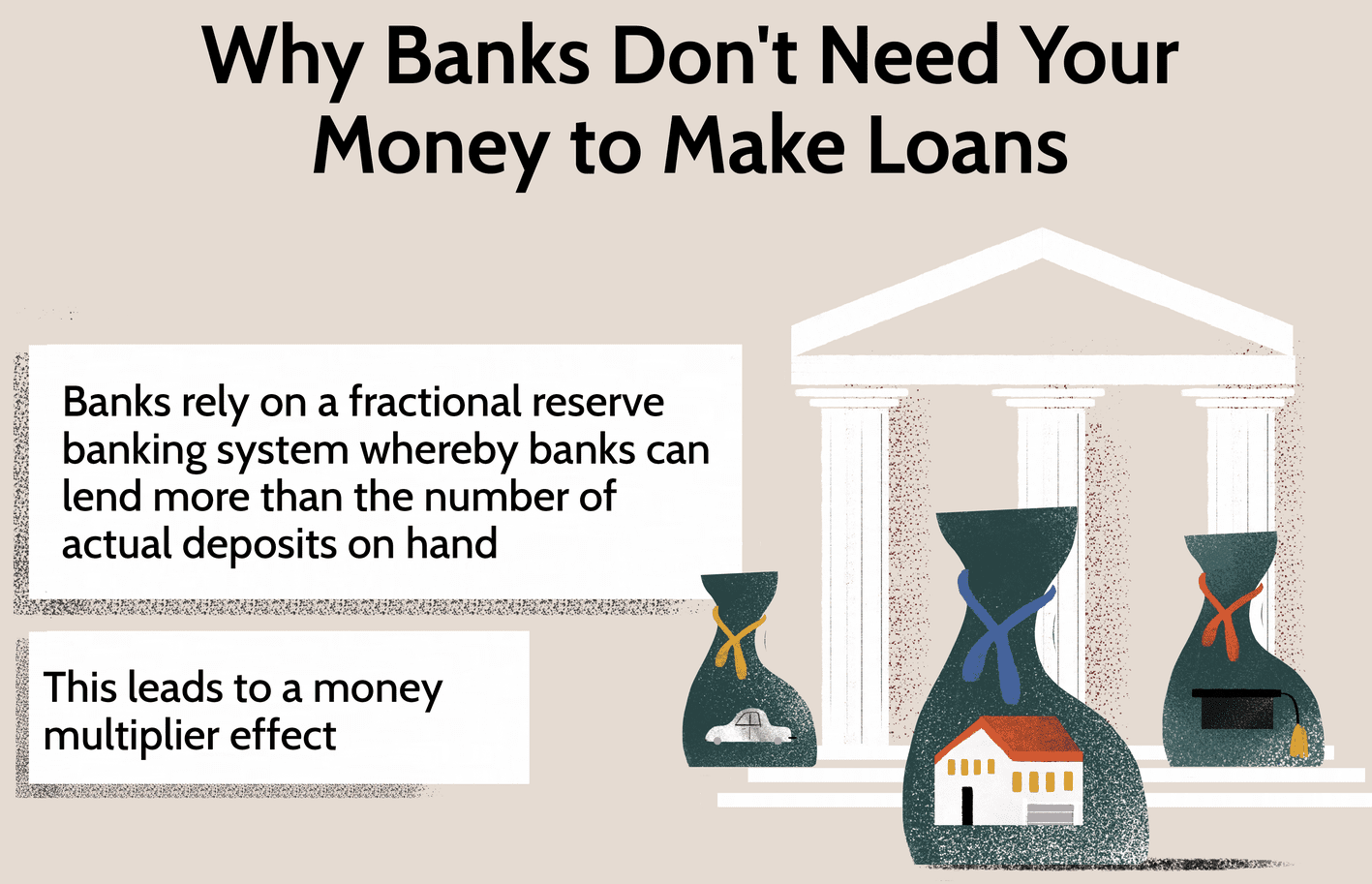

To illustrate this concept further – when you deposit funds into your account at a bank (be it checking or savings), these deposits then serve as resources that can be lent out to other customers seeking mortgages or business loans. Herein lies one way how banks make profit – by charging higher interest rates on these loans than what is paid out to depositors.

Investment Banking

Moving beyond traditional consumer-focused facilities such as lending money or managing transactions via debit card services, we delve into another domain known as investment banking where big deals transpire.

Investment banking, a global leader within this sector, provides wealth management solutions along with M&A advisory roles that bring about substantial income streams.

By grasping these basic principles behind how both commercial and investment facets contribute towards generating profits while providing value-added benefits back to us consumers.

Understanding this helps comprehend why they’re so integral within our society’s economic framework.

Whether handling everyday transactional needs via checking accounts or guiding massive corporates towards profitable decisions through strategic advisory roles – every service offered contributes toward making them central pillars supporting our economies. This article doesn’t cover ways technology has transformed modern-day banking enabling new channels like digital wallets/wire transfer facilities etc., but stay tuned for more insights.

Commercial Banking: A Key Revenue Generator

The landscape of commercial banking is a rich source of revenue for banks. The bulk of their income stems from net interest margin and fee-based services.

Demystifying Net Interest Margin

To comprehend how banks accumulate profits, it’s essential to understand the concept of net interest margin. Net interest margin refers to the discrepancy between what banks charge for loans and what they offer in terms of payouts on deposits.

Banks essentially earn by lending at higher rates than those offered to depositors. Consider this scenario – you make a $1000 deposit in your Wells Fargo checking account, receiving an annual return rate around 1%. Wells Fargo then lends these funds to another customer charging anywhere between 4% up till even 30%, depending upon factors like risk profile, loan tenure, etc.

This differential or spread enables them to cover operational costs while ensuring profit margins are intact. Amidst ever-changing market conditions impacting both borrowing as well as lending rates, maintaining robust net interest margins remains a continuous endeavor for all major players within the banking sector, including central banks and credit unions alike.

Fees-Driven Income in Commercial Banking

Apart from earning through spreads over loans against deposits, commercial banks also draw significant revenues via various fees charged for diverse services rendered ranging from monthly maintenance charges levied on savings accounts or current accounts; interchange fees earned every time customers swipe their debit cards at merchant outlets; wire transfer facilities such as ones provided by US Bancorp; overdraft penalties when clients withdraw more than the available balance in their bank account, amongst others.

All these components add significantly towards enhancing overall earnings, thereby contributing positively towards bottom line figures reported annually by most established names across the global banking industry.

Investment Banking – The Unseen Powerhouse of the Financial World

Investment banking is a realm that operates beyond the borders of traditional commercial banking. It provides specialized financial services, with giants like Goldman Sachs and Morgan Stanley leading the charge.

The Influence of Advisory Fees in Investment Banking

An integral part of an investment bank’s revenue comes from advisory fees. These are levied for offering expert counsel on complex transactions such as mergers or acquisitions, corporate restructuring, among others.

This fee-based income plays a pivotal role in bolstering an investment bank’s earnings. Companies seeking advice on large-scale transactions or strategic decisions turn to these banks due to their deep-rooted expertise and robust network connections within industry circles. Take into account situations where companies plan for mergers; they require professional guidance navigating intricate legalities, valuation considerations, and negotiation strategies, which is exactly what investment bankers offer, thereby earning substantial advisory fees in return.

Raising Capital Through Underwriting Securities

Besides playing advisory roles, underwriting securities forms another significant way how investment banks make money by raising capital through issuing new securities like stocks or bonds, etc., into markets on behalf of clients.

A common form involves Initial Public Offerings (IPOs), wherein shares get sold first to institutional investors followed by retail ones. In exchange for managing this process efficiently while bearing associated risks involved during sale proceedings, the bank charges underwriting fees, adding considerably towards its revenues, especially when dealing with high-value IPOs.

Wealth Management Services – Serving High Net Worth Individuals And Institutions

Last but not least, wealth management too forms a key aspect within an investment bank’s portfolio offerings, catering primarily towards high net worth individuals (HNWIs) and institutions, helping them manage their wealth effectively using various financial tools, thus generating considerable revenues via asset management fees, etc.

This diverse range offered across different revenue streams helps protect against downturns affecting any particular segment while providing growth opportunities across others, making it crucially important

The Power of Interest Income

Commercial banks make money primarily through interest income, a revenue stream that relies on the basic principle of borrowing low and lending high. This involves offering depositors an interest rate for their savings or checking accounts, then loaning these funds out at higher rates.

This system doesn’t just allow your deposited capital to sit idle in a bank account; it actively contributes to financial services such as personal loans, mortgages, and business loans provided by the bank.

Lending Money – The Core Business Model of Banks

Banks’ primary function is accepting deposits and providing loans. When you put your money into a savings account with any commercial banking institution, it forms part of the pool used for various types of credit facilities offered by them.

In fact, when you take up something like an auto loan from your local bank branch or even apply online for home mortgage financing options available via digital wallets enabled due to modern technology advancements within US Bancorp, some portion might be funded using other customers’ deposits.

Understanding Loan Interest Rates and Their Impact on Bank Profits

Determining competitive yet profitable loan rates significantly impacts how much profit banks can generate from this core service they provide. The rate of interest charged on loans is contingent upon several elements, such as the borrower’s credit score and prevailing market conditions.

Banks must ensure they’re charging enough above their cost (the depositor’s rate) so as not only to cover operating expenses but also to turn over decent profits.

Maintaining a Healthy Net Interest Margin (NIM)

A healthy net interest margin – which refers to the difference between the amount earned through interests charged on different kinds of money lent out versus what gets paid back to those who’ve deposited funds with them – becomes a crucially important factor determining profitability for all banking institutions, whether small community establishments or large multinational entities alike.

An optimal balance between risk management strategies against potential defaults along suitable pricing models ensures robust profit margins, thereby securing steady revenues even during challenging times where central banks may adjust official cash rates impacting the overall economy.

How Interest Rates Influence Bank Revenue

The profitability of banks is greatly impacted by interest rates. The net interest margin, the contrast between what a bank earns from loaning out money and what is paid to depositors, is significantly impacted by changes in interest rates.

This might seem counterintuitive at first glance as falling interest rates could mean reduced earnings from loans. However, when managed effectively by banking giants like Bank of America, this can lead to increased revenues too.

Falling Interest Rates: A Blessing In Disguise?

In environments where there are low interest rates, borrowing becomes more attractive due to lower costs. Individuals and businesses alike seize such opportunities for various purposes – be it buying homes or expanding business operations, respectively. The surge in loan demand allows banks not only to make up for decreased rates through volume but also to earn significantly more overall, despite individual loan yields being lower.

Apart from stimulating borrowing activity, declining interest rates often drive investors away from bonds that yield less and towards equities instead. This benefits banks that have robust wealth management divisions managing portfolios invested heavily in stocks rather than fixed income securities.

Balancing Act: Managing Rate Risk

While changes in interest rates impact bank revenues substantially – both positively and negatively – they introduce significant risks known as ‘interest rate risk’. Maximizing returns without exposing themselves excessively to potential adverse movements requires careful asset-liability management strategies involving balancing the duration (or sensitivity) of assets and liabilities, ensuring stable earnings even during fluctuating market conditions.

Capital Markets-Related Income – An Unstable Yet Profitable Source

Banks, like other businesses, have multiple revenue streams. One of these is capital markets-related income. This category includes sales and trading activities, underwriting services, and mergers & acquisitions (M&A) advisory.

Sales and Trading: The High-Stakes Game

In the realm of sales and trading operations within financial institutions such as JPMorgan Chase, securities are bought from one party to be sold to another at a profit margin. It’s akin to playing a high-stakes game where market expertise can lead banks towards significant profits or losses.

The goal here is simple – buy low-priced securities that show potential for growth in value over time then sell them when their prices peak. However, this requires not just knowledge about industry trends but also an understanding of global economic conditions which makes it both challenging yet rewarding.

Underwriting Services: A Balancing Act Between Risk And Reward

Apart from sales and trading activities, banks earn money through underwriting services too where they act as middlemen between companies issuing new stocks or bonds looking for investors willing to purchase them.

JPMorgan Chase, known for its prowess in managing initial public offerings (IPOs), takes on considerable risk during this process because if there aren’t enough buyers interested at the proposed price point, they may end up holding onto unsold inventory.

This balancing act between risk versus reward contributes significantly towards making money earned by investment banking divisions within large commercial banks.

Mergers & Acquisitions Advisory: Navigating Complex Business Transactions

Navigating complex business transactions like mergers with other firms or acquiring smaller companies falls under M&A advisory offered by many major financial institutions including Goldman Sachs.

These transactions command hefty fees due to their complexity involving regulatory hurdles along with intricate financial structuring needed throughout the deal-making process.

However, similar to other capital markets-related income sources discussed earlier, even though lucrative opportunities exist here, there’s always inherent instability since overall profitability depends heavily upon fluctuating market

Not All Banks Are Created Equal – Different Ways Banks Generate Revenue

Banks can vary greatly in their structure and purpose, making them unique. Each type of bank has its unique way of generating revenue, which can be categorized into three main types: commercial banks, investment banks, and universal banks.

The Commercial Banking Model

Commercial banking institutions primarily focus on deposit-taking from customers and lending money back out at higher interest rates. The net interest margin (NIM), a measure that represents the difference between what they earn as loan interests versus what they pay to their depositors, forms their primary source of income.

Banks like Wells Fargo, for instance, rely heavily on this model, with additional revenues coming through various fees such as account maintenance charges or overdraft fees.

Making Money Through Investment Banking

Differentiating itself from traditional banking is investment banking firms such as Goldman Sachs. These entities specialize in providing services including mergers & acquisitions advisory or underwriting securities, which help businesses raise capital. Their key sources of income include advisory fees charged for offering expert advice during large corporate transactions, along with trading revenues derived from buying/selling securities.

A Blend Of Both Worlds – Universal Banking Model

Last but not least are the universal models followed by giants like JPMorgan Chase. Combining both commercial and investment operations under one roof allows these kinds of establishments to diversify their revenue streams significantly. This approach enables them to leverage synergies across different business lines while reducing risk exposure associated with relying solely on either traditional or investment banking activities.

All said, it’s important for investors looking at bank stocks or entrepreneurs planning new ventures in this sector to understand how each kind works before making informed decisions.

Credit Unions Vs Banks – A Comparative Analysis

Choosing between a credit union and a traditional bank often comes down to individual financial needs. Both offer similar services, such as checking accounts, savings accounts, loans and credit cards; yet the way in which these two types of institutions operate is quite different. However, the business models of these two types of institutions vary greatly.

Understanding Credit Union Operations

A key distinguishing feature is that Credit unions, unlike banks, aim to maximize corporate profits for shareholders who may not even use their banking services. Credit unions, on the other hand, are member-owned cooperative entities operating on a non-profit basis with an intent to serve members rather than generating profit.

The democratic nature means each member has an equal say in electing the board, regardless of the amount deposited or borrowed from the union. This ensures that all stakeholders are represented in the decision-making process, unlike traditional banking which is usually dictated by a select few. This is something rarely seen in the commercial banking world, where major policy matters are typically decided by a small group of top executives and shareholders only.

Differences In Financial Products And Services Offered

Banks tend to offer a diverse range of financial products, including those related to investment banking. This is something that is hardly found in most credit unions. Primarily, credit unions stick around core consumer-focused offerings, limiting the choices and options available to consumers, especially those looking beyond just basic retail banking needs in areas like wealth management. Thus, it is not a matter of superiority but rather that they serve distinct groups of customers based on their particular needs and inclinations. Hence, potential users need to conduct thorough research before deciding to park funds in either type of institution.

Decoding the Financial World: How Do Bankers Make Money?

Uncover the mystery of how bankers make money. Explore commercial banking, investment strategies, and the role of interest rates in our latest post.

Financial Planning – Helping Clients And Generating Revenue For Banks

The banking sector’s approach to financial planning serves a dual purpose. It not only aids clients in efficiently managing their finances but also acts as a revenue stream for the banks themselves.

Serving Client Needs Through Financial Planning

Essentially, financial planning is about guiding individuals and businesses on how best to manage their money earned from various sources such as salaries or side hustles. This includes budgeting, future expense forecasting, smart investing strategies, and preparing for retirement or other significant life events.

Banks typically offer these services within their product suite with an aim of attracting more customers while helping them make informed decisions regarding the effective use of funds.

Revenue Generation through Financial Advisory Services

Apart from enhancing customer satisfaction and loyalty by providing value-added services like this one, offering personalized advice on investment strategies can be quite profitable too.

This is because most commercial banks charge advisory fees when they create comprehensive individualized plans tailored towards specific client needs. JPMorgan Chase, Bank of America, and others are well-known within industry circles for earning substantial revenues via non-interest income streams, including account fees charged across checking accounts, among others, besides interest incomes accrued over loans disbursed and savings deposits collected.

Impact of Technology on Modern-Day Banking

The banking industry has undergone a massive transformation, thanks to technology. New platforms such as digital wallets and wire transfer facilities have opened up fresh avenues for banks to generate revenue.

Digital wallets have become a major development in the recent past, allowing people to store their money digitally without having to possess a standard bank account and enabling them to make transactions anytime from anyplace. They offer users an easy way to store money digitally without needing a traditional bank account, enabling transactions anytime from anywhere.

Banks like US Bancorp, which provide these services, earn income through transaction fees each time customers use their platform for payments or transfers.

The Influence of Online Banking on Revenue Generation

Online banking is another major innovation that’s reshaping how financial institutions operate. It allows customers to access and manage their accounts remotely via computers or mobile devices – convenience at its best.

This service not only enhances customer experience but also reduces operational costs associated with maintaining physical branches – savings that can be redirected towards other profit-making activities within the institution.

Mobile Apps and Their Role in Today’s Banking World

With increasing smartphone usage worldwide, mobile apps have become indispensable tools in modern-day banking. Through these applications, banks provide various services including fund transfer facilities, earning them wire transfer fees every time a customer sends money domestically or internationally using this feature.

The reduced need for paper-based operations due to digitization leads to cost-savings, further contributing positively towards overall profitability by cutting down overheads while enhancing efficiency.

Fintech Partnerships: A Profitable Strategy for Banks

An emerging trend among forward-thinking financial institutions involves forging partnerships with fintech companies offering innovative solutions aimed at improving user experience while boosting bank revenues simultaneously. Banks partner with fintech firms providing payment processing services, thereby facilitating seamless transactions across different channels leading to increased interchange fee incomes.

This mutually beneficial relationship between banks and fintech companies creates win-win scenarios where both parties benefit financially, delivering superior value propositions to end-users.

FAQs in Relation to How Do Bankers Make Money

Do bankers make a lot of money?

Yes, banking can be lucrative. However, earnings vary widely depending on the banker’s role and experience level.

Why do bankers make so much money?

The high pay in banking often reflects the complex nature of their work, long hours, and significant responsibilities tied to managing large sums of money.

How do banks mainly make money?

Banks primarily generate revenue through interest income from loans and various fee-based services like account fees or credit card charges.

What are the 4 ways banks make money?

Banks earn via net interest margin (difference between loan rates and deposit rates), fees for services rendered, advisory roles in investment banking, and capital markets-related activities such as trading securities.

Conclusion

Banking, a complex yet fascinating world of finance, has intrigued us all.

We’ve uncovered how bankers make money through various strategies.

The key lies in commercial and investment banking services offered by these financial institutions.

From checking accounts to corporate transactions, banks have diverse revenue streams.

Interest income plays a significant role as banks lend at higher rates than they pay depositors.

Falling interest rates can boost profits for leading institutions like Bank of America or Citigroup.

Banks also rely on fee-based incomes such as credit card charges and account fees.

Different types of banks employ unique approaches to generate revenue depending on their focus areas – be it purely commercial or investment banking or both.

Credit unions differ from traditional banks with their primary aim being covering expenses rather than making large profits for shareholders.

New avenues opened up by technology like digital wallets have transformed modern-day banking adding another dimension to bank revenues.

If you’re keen on exploring more about the financial world and ways to earn money, consider visiting Money Empire. We delve into topics ranging from saving money and business strategies to SEO marketing tactics.

Amazon and the Amazon logo are trademarks of Amazon.com, Inc, or its affiliates.